Lenders Mortgage Insurance (LMI) Waivers for Professionals

LMI waivers let eligible professionals save on home loans by avoiding Lenders Mortgage Insurance costs.

PARTNERSHIP

What is an LMI Waiver for Professionals?

Lenders Mortgage Insurance (LMI) is an additional cost for borrowers taking out a home loan with an LVR (loan-to-value ratio) higher than 80%. This insurance protects mortgage lenders but does not benefit borrowers. The cost of mortgage insurance can be tens of thousands of dollars, making homeownership more expensive.

However, some home loan lenders offer LMI waivers for certain professionals, allowing them to access 90 LVR home loans or 95 LVR home loans without paying LMI. This can significantly reduce the upfront cost of buying a home.

Professions Eligible for an LMI Waiver

The following professions may qualify for an LMI waiver, along with their maximum LVR limits and lenders that offer waivers:

How Much Could My Clients Save?

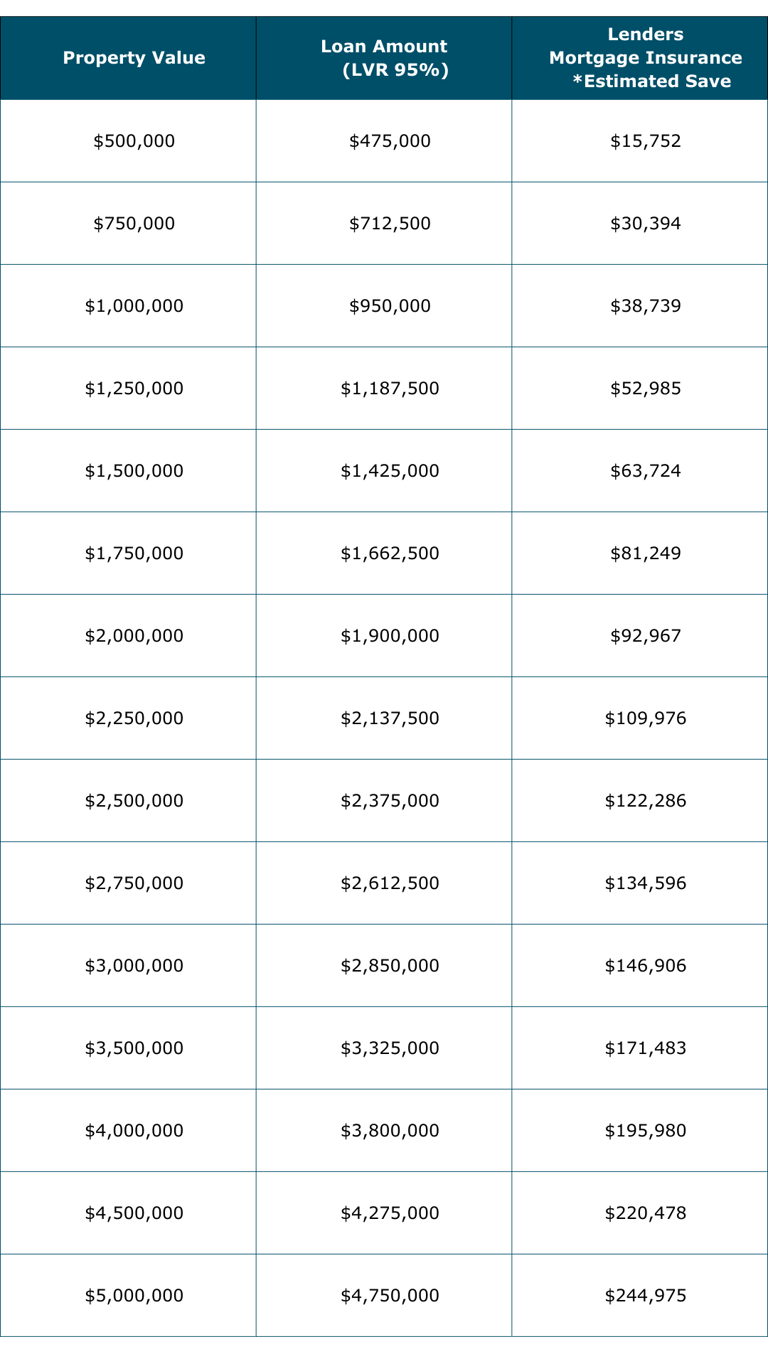

By waiving LMI, you can save tens of thousands of dollars. The exact savings depend on factors like your loan amount and Loan-to-Value Ratio (LVR). Since most medical professionals secure loans with a 95% LVR, here are estimated LMI savings for various property values at this ratio:

Disclaimer: Savings may differ between lenders depending on which LMI insurance provider they use.

How to Apply for an LMI Waiver

Check Eligibility: Verify if your profession qualifies and if you meet income requirements.

Compare Lenders: Not all mortgage lenders offer LMI waivers for every profession.

Calculate Savings: Use an LMI calculator to determine how much you’ll save.

Submit Your Application: Provide proof of income, employment, and professional registration.

Loan Approval: If approved, you’ll receive competitive home loan rates without LMI.

Alternatives to LMI Waivers

First Home Guarantee (FHBG): Allows first-home buyers to purchase with a 5% deposit and no LMI.

Guarantor Loans: A family member acts as security, reducing LMI costs.

Saving a Larger Deposit: A 20% deposit eliminates the need for LMI.

Refinancing Home Loans: Switch to a lender offering lower rates and no LMI.

Disclaimer: The opinions expressed in this article are strictly for general informational and entertainment purposes only and should not be taken as financial advice or recommendations. While every effort is made to ensure the listed offers are accurate, we make no guarantee regarding their accuracy, completeness, or availability.

Made by advisors, for advisors.

DISCLAIMER: The information provided on this website is general in nature and is not intended to be specialist or personal advice. The information provided on our website has been prepared without taking into account your objectives or financial needs. You should consider the appropriateness of the advice to your own situation before taking any action. The information provided should not be relied upon for the purposes of entering into any legal or financial commitments. Specific investment advice should be obtained from a suitably qualified professional. If any financial product has been mentioned, you should obtain and read a copy of the relevant Product Disclosure Statement and consider the information contained within that Statement with regard to your personal circumstances before making any decision about whether to acquire the product. You can obtain a copy of the Product Disclosure Statement by speaking to a member of our team.

The advice provided in marketing material and posts by Cromeloan, our representatives and our partners is to be considered general advice only. It has been prepared without taking into account your specific objectives, financial situation or needs. Before acting on this advice, you should consider the appropriateness of the advice having regard to your own objectives and financial needs. If any products are detailed in this presentation, you should obtain a Product Disclosure Statement relating to the products and consider the information provided before making any decisions.

Craggle Services Pty Ltd (trading as Cromeloan) ABN 33 676 327 272 is a Credit Representative (540988) of Home Mortgage Plus Pty Ltd ACN 105 991 839 (ACL 392200)